How Seattle Agents Win More Listings With a Contingency-Free Buy Before You Sell Program

Read more

.webp)

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

In most housing markets, buying before you sell is a straightforward process.

You find the move-up home you want, make an offer with the contingency that your current home will sell, and by the time everything settles you’ve got a buyer for your old home and an accepted offer for your new one.

Unfortunately, Seattle's market conditions make that approach seemingly impossible.

Homes here receive multiple offers within days of listing, often within hours. With the average Seattle home price hovering above $850,000 (as of writing, June 2026), sellers routinely choose buyers who are ready to close over those whose offer depends on selling their current home first.

That’s not the only problem with a contingency offer.

It also puts you in a position in which you have to sell fast to meet the condition in your offer.

When you're forced to sell under a deadline — rushing to close on your current home fast enough to fund the next one — you hand the buyer across the table a lot of leverage.

They know you can't afford to wait. So they come in low, push back on inspections, and you take it because the clock is running.

On an $850,000 home, that can mean tens of thousands of dollars in lost value.

Seattle's Mortgage Broker's Contingency Buster Program solves the contingency problem before you ever write an offer.

Instead of a bridge loan, a home equity loan, or asking a seller to wait on your current home to sell, the program places a guaranteed buyer on your current home first.

Your exit is secured before your entry begins.

Because the sale of your current home is no longer dependent on timing or a contingent offer chain, you can make a clean offer on the next home with no home sale contingency attached.

In a market where sellers are regularly choosing between multiple bids, that's frequently the difference between a competitive offer that wins and watching someone else close on the home you wanted.

That's the primary benefit, and it's the one most people come looking for.

But there's a second benefit attached to selling your existing home that tends to go unnoticed.

Getting the time to stage and sell your home without having to make two mortgage payments and still avoid temporary housing is incredibly valuable for most Seattle homeowners.

The moment you go into contract on your next home with a contingency, a clock starts.

You now need to sell your current house fast enough to fund the down payment, satisfy lender requirements, and avoid carrying costs on two properties at once.

That deadline doesn't just create financial pressure. It changes your entire position as a seller.

Under normal conditions, a seller has leverage.

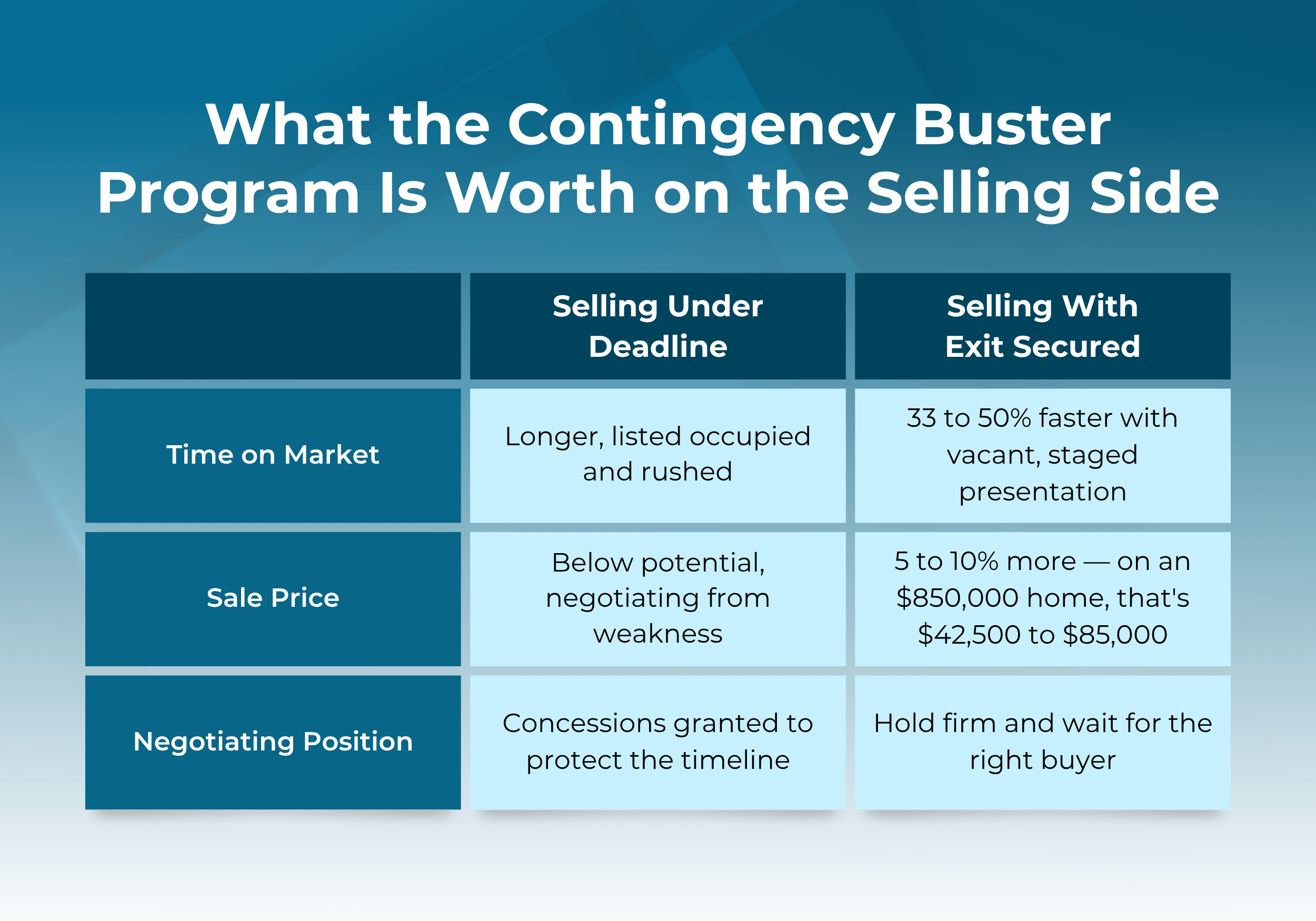

They can wait for the right buyer, push back on lowball offers, hold firm on inspection concessions, and time the listing to maximize presentation and foot traffic. They're in control because they have options.

A seller with a deadline has fewer options, and the buyer sitting across the table will take advantage. A deadline-driven seller is a readable seller, and buyers price that in.

What most people don't account for is how much that pressure actually costs once a buyer shows up:

Because the Contingency Buster Program places a guaranteed buyer on your current home before you go looking for the next one, there's no deadline forcing the sale. That changes everything about how the transaction unfolds.

You have time to vacate the property and stage it properly. You can hold out for the right offer, push back on inspection demands, and present the home as a vacant, staged property rather than an occupied one. The program also gives you flexibility around the closing date, and in cases where timing requires it, a rent back agreement can cover the gap between closings.

With a committed buyer already in place, you're no longer selling because you have to. You're selling because you're ready, and that distinction changes how every negotiation unfolds.

Staged homes sell 33 to 50% faster and for 5 to 10% more than comparable unstaged homes. On an $850,000 home, that's $42,500 to $85,000 in your current home's equity that a pressured sale would have left on the table.

You have to have two things to capture full value for your home, and they're both harder to achieve when you're selling under pressure.

The first is presentation.

When you're not racing to meet a contingency deadline, you have the option to vacate before listing. A vacant home can be fully staged, photographed at its best, and shown without the clutter and evidence of daily life that makes it harder for buyers to picture themselves in the space.

That kind of presentation commands attention and it's only available to sellers who aren't under pressure to move fast.

The second is patience.

A seller without deadline pressure can hold out for the offer the home actually deserves. A seller with a contract pending on their next house often can't afford to wait, so they take what's in front of them rather than what the home is worth.

When you have both, you get full price control. A home that photographs well, shows cleanly, and has time to attract serious buyers commands a better price than one that's listed quickly, occupied, and pulled before the right buyer ever saw it. Take away either one and you're leaving money on the table.

Homeowners buying and selling simultaneously without a structured exit absorb losses on both ends, and rarely see the full number until the dust settles.

On the purchase side, a contingent offer hands the seller a reason to choose someone else. In a multiple-offer situation, a lower bid from a clean buyer routinely beats a higher one that depends on another transaction closing first.

On the sale side, the deadline produces exactly what the previous section describes: a rushed listing, an occupied home that can't compete on presentation, and accepted offers that don't reflect what the home was actually worth.

A homeowner who overpays on the next house while underselling the old one has absorbed a double penalty for a sequencing problem that was completely solvable. The homeowners who avoid it are the ones who structured the exit first.

There's a third benefit worth mentioning for homeowners thinking beyond the immediate transaction.

Once you've closed on your new home and secured your new mortgage, Seattle's Mortgage Broker's Step Down Refinance Program gives you a built-in strategy to reduce your monthly mortgage payments over time without adding to your loan balance.

Rather than relying on a home equity line of credit, bridge financing, or short term financing to manage the transition between properties, you enter the new loan already positioned to refinance incrementally as interest rates drop without stacking total loan costs onto your balance, a second mortgage, or disruption to your debt to income ratio.

For homeowners in a competitive real estate market who stretched to win the right home, that kind of financial flexibility is what happens when careful planning pays off.

Homeowners don’t always think about the selling side until they're already under contract on the next home.

By then, the deadline is already running and the leverage is already gone.

The Contingency Buster Program changes the opportunity entirely.

When the guaranteed buyer is in place before you make your first offer, you go into the purchase clean and into the sale negotiating from strength. There’s no rush to take a low-ball offer; no need to list an unstaged home.

That's how you stop leaving money on both ends of the transaction.

Talk to Seattle's Mortgage Broker about the Contingency Buster Program and start your next move from a position of strength.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)