How Seattle Agents Win More Listings With a Contingency-Free Buy Before You Sell Program

Read more

.png)

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

You found the home. The price works. The neighborhood is right. You make an offer on a real estate opportunity you thought was yours. And then you lose your dream home.

It’s not because your number was wrong or you weren't qualified, but because your offer carried a condition the seller had no reason to accept.

That's the reality of a home sale contingency in Seattle's real estate market. It doesn't automatically disqualify you, but it does give the seller a reason to choose someone else.

In a competitive market where strong homes attract multiple offers, that reason is often all a seller needs to move on to the next bid.

Most buyers assume they have no choice. They believe that the home sale contingency is required if they haven't sold yet.

It's not.

The sell-first condition attached to your offer is a variable you can control, and removing it changes how sellers view your bid entirely.

When your offer arrives with a home sale contingency, the seller sees a buyer who wants the home, maybe even at a competitive price. But they also see a deal that depends on a second transaction closing first, one they can't control and have no reason to trust will happen on time.

Here's what that uncertainty looks like from a seller’s perspective:

They don't know if your current home is listed, whether it has serious buyer interest, or how long it will take to close. Accepting your offer means their property goes off the market while all of that plays out. And if your sale falls apart, they're back to square one with less momentum and a listing that now carries the stigma of a failed deal.

That risk is why sellers with options choose the cleaner offer. Not always the higher one, the cleaner one.

When that happens, your search restarts under pressure.

The fallout typically looks like this:

Every option that follows a lost contingent offer is a worse version of the one that came before it.

You started the process qualified and prepared. You end up reactive, and reactive buyers rarely land the home they actually wanted.

A sale contingency can also trigger a kick out clause, which allows the seller to keep showing the home and accept a better offer while your contingency is still active.

If another offer comes in, you may be forced to remove your contingency or walk away, often losing your earnest money deposit in the process. That contingency period, typically 30 to 60 days, is a window of uncertainty no motivated seller wants to sit inside.

Beyond the home sale contingency itself, buyers should understand that most purchase offers include several common contingencies including a financing contingency, a home inspection contingency, an appraisal contingency, and sometimes a mortgage contingency.

Each one adds a layer of risk from the seller's perspective. Removing as many as possible, especially the sale contingency, dramatically strengthens a buyer's offer.

Most homeowners walk away from a lost offer thinking they need to try harder, bid a higher price, time it better, or simply be more patient.

What you actually need is to remove the one condition that made the seller look elsewhere in the first place.

Seattle's Mortgage Broker secures a guaranteed backup purchase contract on your existing home before you make an offer on the next one. That means a committed buyer is already in place before you step into the market.

With that contract in hand, your offer goes in without a home sale contingency. The seller receives a purchase offer backed by certainty, not hope. That's the difference between an offer that gets accepted and one that gets passed over.

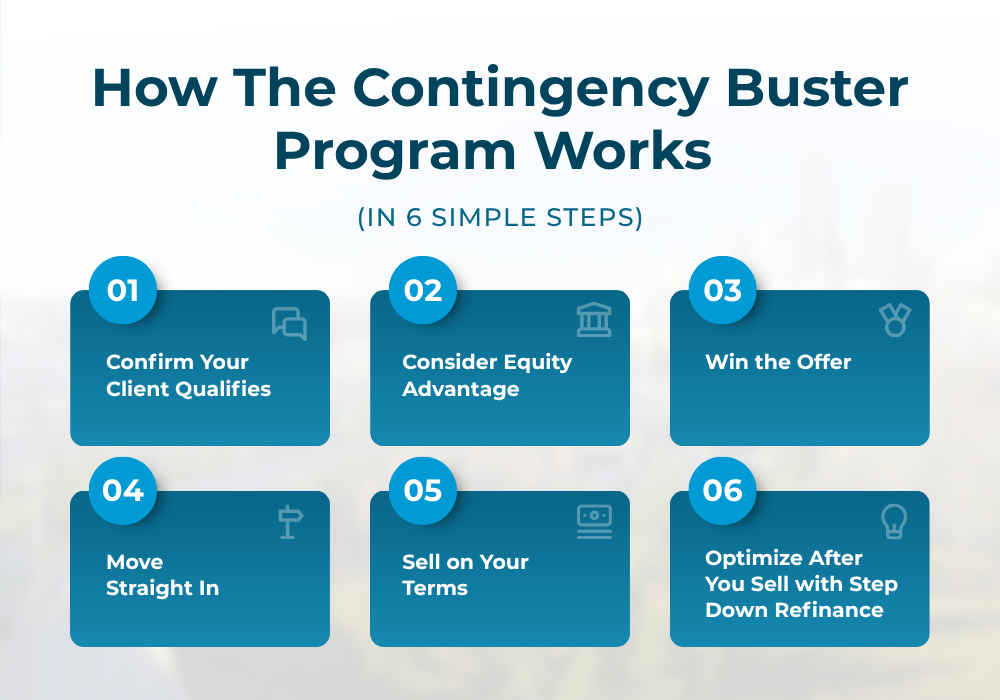

Here's how it works from start to finish:

We confirm you have at least 22% equity in your current home. That's the minimum needed to make the contingency disappear from your next offer.

With the guaranteed backup contract in place, you make an offer without a home sale contingency. The seller sees a buyer who can close, not one who might.

When you win the offer, you close quickly and move straight into your new home. No storage unit. No short-term rental.

Your current home lists vacant, staged, and without time pressure. Staged homes statistically sell 33 to 50 percent faster and for 5 to 10 percent more than comparable unstaged properties, according to the National Association of Realtors’ 2024 Profile of Home Staging.

On a Seattle home, selling for even 5 percent more is meaningful money that goes directly into the equity of your new home.

Once your current home sells, remaining equity gets applied to your new mortgage balance through SMB's Step Down Refinance Program.

That lowers your rate and monthly payment on the home you just won, turning a single transaction into a long-term financial strategy.

Most Seattle homeowners already have the equity needed to buy a house before selling. The challenge is accessing it without taking on a second mortgage payment or a costly bridge loan.

Equity Advantage is an optional add-on to the Contingency Buster Program that lets you unlock up to 75% of your current home's equity before it sells. That advance covers your down payment, closing costs, staging, moving expenses, or debt payoff — whatever strengthens your position as a buyer.

Here's why it’s so much better than a bridge loan:

No monthly payment during the transition.

The advance carries no payment obligation while you own both homes.

Repaid automatically when your home sells.

The full amount is repaid through escrow at closing. You never write a check.

Your budget stays intact.

Because there's no monthly payment, your debt-to-income ratio doesn't take a hit, and your qualification on the new purchase stays clean.

With Equity Advantage in place, you're buying from a fully funded position while your monthly budget stays exactly where it was.

With the Contingency Buster Program, your offer competes like cash. You move once, sell on your terms, and choose your next home deliberately instead of under pressure.

The alternative costs more than most homeowners realize. Temporary housing, rushed decisions, and a lived-in home sold under deadline almost always exceed the perceived risk of buying first.

Homeowners who use the Contingency Buster Program close on the home they wanted and move straight in. Most describe it as the first time a home purchase felt like something they controlled rather than endured.

Sellers choose certainty over everything else.

When you remove the home sale contingency from your offer, you're not just more competitive — you're operating from a position other buyers can't match.

That position is available to you today.

One conversation confirms whether you qualify and shows you exactly what a clean, competitive offer looks like for your situation.

Ready to compete like a cash buyer? Click here to get started.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)