How Seattle Agents Win More Listings With a Contingency-Free Buy Before You Sell Program

Read more

.webp)

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

This article was recently updated on July 29th, 2026.

If the house you love in Seattle costs more than a standard mortgage will cover, you're one of a growing number of buyers running into the same wall.

Rising home prices in Seattle can mean that buyers are financing amounts that fall outside what a conventional mortgage will cover.

When a home's price exceeds the conforming loan limit set for the area, the loan needed to buy it stops qualifying as a standard mortgage and becomes a jumbo mortgage loan instead.

A jumbo loan is a mortgage for an amount above the conforming threshold, with its own rules around down payments, underwriting, and lender risk.

This guide walks through what separates a Seattle jumbo mortgage loan from a conventional one, when you might not actually need one, and what alternatives are worth considering first.

Seattle's housing market has stayed competitive for years, and homes in high-demand neighborhoods routinely draw multiple offers.

That kind of competition pushes prices up, which means the loan needed to buy a home climbs right along with it.

A buyer who might have qualified for a conventional mortgage a few years ago can find themselves needing a jumbo loan simply because the price of a comparable home has increased.

This pattern shows up whenever demand outpaces available inventory, and it's part of why understanding how a jumbo mortgage loan works has become relevant to more buyers than it used to be.

A jumbo mortgage loan is a mortgage that exceeds the conforming loan limit set by the Federal Housing Finance Agency, or FHFA.

Any loan above that threshold cannot be purchased or guaranteed by Fannie Mae or Freddie Mac, the government sponsored enterprises that buy and back conforming mortgages. That's what pushes it into jumbo territory.

Because lenders hold a jumbo loan on their own books and assume all the risk, they apply stricter qualification standards than you'd find with a conventional loan.

Despite the name, "jumbo" doesn't necessarily mean unaffordable.

That threshold isn't the same everywhere, and Seattle's location plays a direct role in where it lands.

The FHFA doesn't set one flat conforming loan limit nationwide. It sets a base limit and a higher ceiling loan limit for high cost areas, where average home prices run well above the national baseline.

King County is one of those high cost areas, which is part of why the conforming threshold here sits above the national figure.

Because maximum loan amounts vary by county, a jumbo threshold in King County can look very different from one in a rural county elsewhere in the state. Current conforming loan limits for King County are published annually by the FHFA and adjust each year with home price changes nationwide. Check the latest figure before assuming last year's threshold still applies.

Conforming loan limits are about the loan amount you need, not the purchase price of the home.

If you can keep the amount you borrow under the conforming threshold, you may not need a jumbo mortgage loan at all, even on an expensive home. The lever that decides this is your down payment, which we'll cover in more detail below.

The loan amount is what typically separates a jumbo loan from other types of home loans, but it's not the only difference.

Because these loans carry more risk for lenders, a jumbo loan can be harder to find, require a bigger down payment, come with a tougher bar to qualify, price differently on your rate and payment, and put you through stricter underwriting. Here's what to expect on each.

Jumbo loans aren't always as widely available as conventional loans. Because a lender is taking on a larger amount with a single borrower, they view jumbo lending as higher risk.

During periods of economic uncertainty, mortgage lenders may raise qualification requirements, price in that added risk, or temporarily pull back on jumbo lending altogether, similar to what's happened with home equity lines of credit in the past.

Not all jumbo lenders apply the same standards, and national names like Rocket Mortgage set their own guidelines separate from what a local broker can offer. Availability is worth checking early, before you assume a jumbo mortgage loan is guaranteed to be an option.

Jumbo loans typically require a larger down payment than a conventional loan does.

The exact amount depends on the lender, your credit profile, and the size of the loan, and it tends to climb further for second homes, investment properties, or multi-family purchases. There's no single fixed number here. It varies enough by lender that it's worth confirming directly rather than assuming a standard figure applies.

Lenders set a minimum credit score for jumbo loans that typically run higher than what a conforming mortgage requires. They also look closely at your debt to income ratio, since jumbo underwriting leaves less room for a stretched budget, and they weigh how much existing mortgage debt you're carrying relative to your income.

Cash reserves matter too. Lenders often want to see savings beyond your down payment and closing costs, since a jumbo loan carries more risk if your income changes. Underwriting on a jumbo loan is really an assessment of your overall financial health, not one single number.

Mortgage rates on a jumbo loan don't automatically run higher than a conforming one. Pricing depends on the lender, your qualifications, and where the interest rate market sits at the time you lock.

What matters most for your monthly payments is the combination of loan amount, mortgage interest rate, and term. A larger loan at a comparable rate still means a larger payment, so it's worth comparing more than one lender before you commit. Because loan amounts are bigger, mortgage interest deductions can also work differently on a jumbo loan than on a conforming one, and it's worth asking a tax professional how that applies to your situation.

Because jumbo loans are larger and riskier, lenders apply stricter underwriting standards, including:

Each of these can add friction to closing on a jumbo loan, from a lower ceiling on lender options to a longer list of documents to produce. None of it applies if you can stay under the conforming limit, which is why the alternatives below are worth ruling out first.

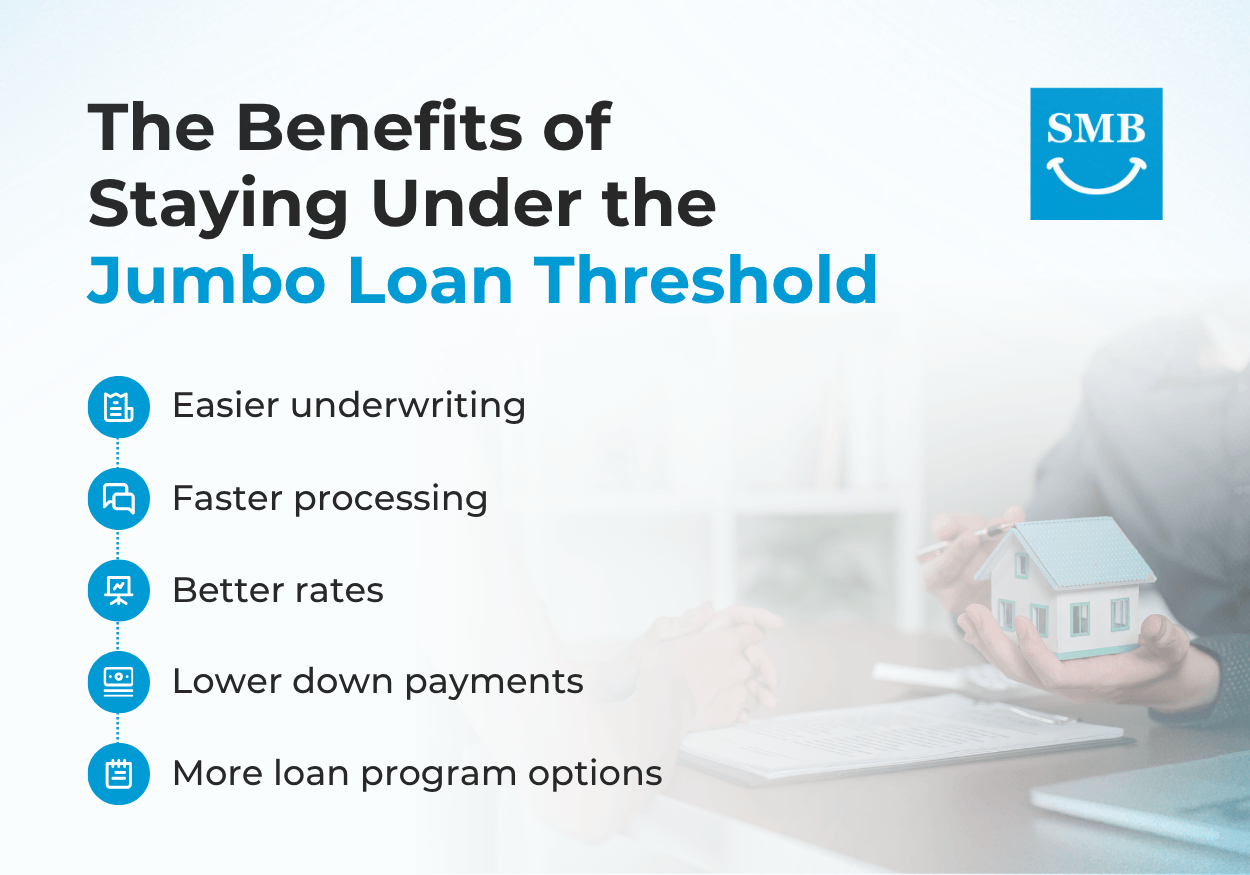

A jumbo mortgage loan isn't always the right path, and there are advantages to staying under the conforming limit when it's possible: easier underwriting, faster processing, often better rates, lower down payments, and more loan program options to choose from.

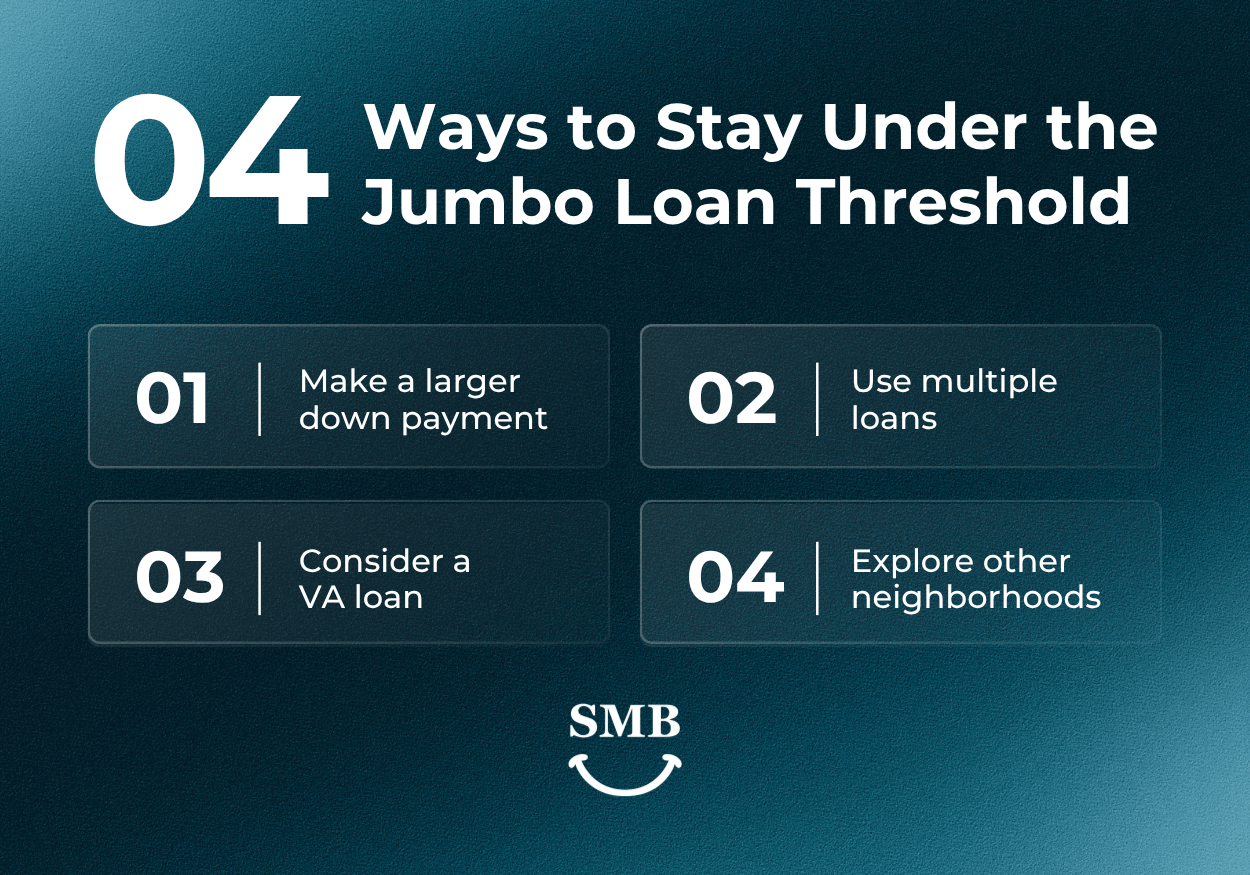

If you'd rather avoid a jumbo loan, or if a high debt-to-income ratio or lower credit score makes qualifying harder, here are the paths worth exploring first.

The loan amount is what matters, not the price of the house.

You can pursue a more expensive home and still stay under the conforming limit, as long as the difference is covered by a larger down payment. This route works well for buyers who can save more upfront in exchange for avoiding a jumbo mortgage loan altogether.

Some buyers split their financing into two loans instead of one, keeping the primary mortgage under the jumbo threshold and covering the rest with a second loan alongside their down payment. This structure is often called a piggyback loan.

VA loans follow their own rules. Eligible veterans and service members can often borrow above the conforming limit without the same down payment and reserve requirements that apply to a standard jumbo loan, so it's worth asking whether this option applies to you before assuming a jumbo loan is the only path.

Seattle's suburbs and surrounding areas often offer more home for the money than the city center does.

Some buyers widen their search to areas outside Seattle proper to find a better fit for their budget without needing a jumbo loan. The right move is to separate what you're unwilling to compromise on from what you can flex on, then use that list to guide where you look next.

Avoiding a jumbo loan often comes down to matching your purchase to the right loan product.

Seattle's Mortgage Broker's High Balance program is built for exactly this and covers loan amounts from $766,550 up to the county loan limit, with a 5% down payment able to stretch as high as $1 million in King, Pierce, or Snohomish counties. That's a higher price point than most buyers realize is still available outside jumbo underwriting.

If you're a first-time buyer, our Conventional Loan program allows as little as 3% down, which can also help keep your loan amount under the conforming threshold on a lower-priced purchase.

We look at your full picture, including your down payment, your target price, and which of these products fits, before you make an offer. That way you're not defaulting into a jumbo loan simply because no one checked whether a High Balance or low-down-payment option would work instead.

A jumbo mortgage loan can be the right call, but it isn't the only call.

Whether you need a jumbo loan or can stay within conforming limits depends on the home you want, your down payment, and your financial picture. That's a conversation worth having before you assume either path is your only option.

Not sure which side of the threshold you land on? Schedule a strategy call to find out before you make an offer.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)