How Do You Buy Another House Before Selling Yours Without Losing $40K?

Read more

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

You've been in your home long enough to know when it's time to move.

The neighborhood was great when you bought it, but life looks different now. Maybe the commute changed, your family grew, or you've simply outgrown the space.

You've done your research and you know what you want in your next home and roughly what you can spend.

Then the reality of the Seattle market sets in.

It doesn't take an experienced real estate agent to see that you can't make a move on a new home until you know what your current home will sell for. The default move is a contingency offer, a condition that ties the deal to your current home selling first. It sounds reasonable.

But in Seattle's market, a contingency attached to your offer tells sellers their sale depends on a transaction they have no control over. In a competitive market, that's enough to get passed over.

You can do everything right, get mortgage preapproval, time your move around a buyer's market, prepare for the financial realities of the transition, and still lose the home you wanted because your offer arrived with a sell-first condition that gave the seller every reason to choose someone else.

That's the problem the Contingency Buster Program from Seattle’s Mortgage Broker was built to solve.

Through this program, we secure a guaranteed purchase contract on your current home before you make an offer on a new one. The sell-first condition you would have needed to include on your offer is no longer necessary.

No contingency. No uncertainty for the seller. No reason to pass you over for a cleaner bid.

And it also means no temporary housing or rent back agreement.

Here's exactly how it works.

Before you can make any move, you need to know exactly how much equity you have in your home.

A minimum of 22% home equity line is the threshold that qualifies you for the Contingency Buster Program, and with it, the ability to remove the sell-first condition from your next offer entirely.

Once Seattle's Mortgage Broker confirms your equity position, we’ll map your path forward from there.

What you find in this step determines everything that comes after it.

Now that your equity position is confirmed and you're above that 22% threshold, you're eligible for the Contingency Buster Program.

This is where the process shifts in your favor.

Seattle's Mortgage Broker places a guaranteed purchase contract on your existing home before you make an offer on a new one. Not a listing. Not a maybe. This gives you a committed buyer already in place before you enter the market.

That contract is what makes the sell-first condition disappear from your offer.

In Seattle's real estate market, sellers aren't just choosing the highest bid, they're choosing the buyer who represents the least financial risk.

With a guaranteed contract already in place on your current home, your offer can compete with cash offers on equal footing. No second transaction to wait on. No uncertainty about what happens next. No reason to choose anyone else.

In a market where strong homes draw multiple offers, that's the difference between winning and being passed over.

You've got a guaranteed buyer lined up on your current home and you know your equity position. Then the next question hits. Where is the down payment coming from?

This is where Seattle's Mortgage Broker's Equity Advantage Program comes in.

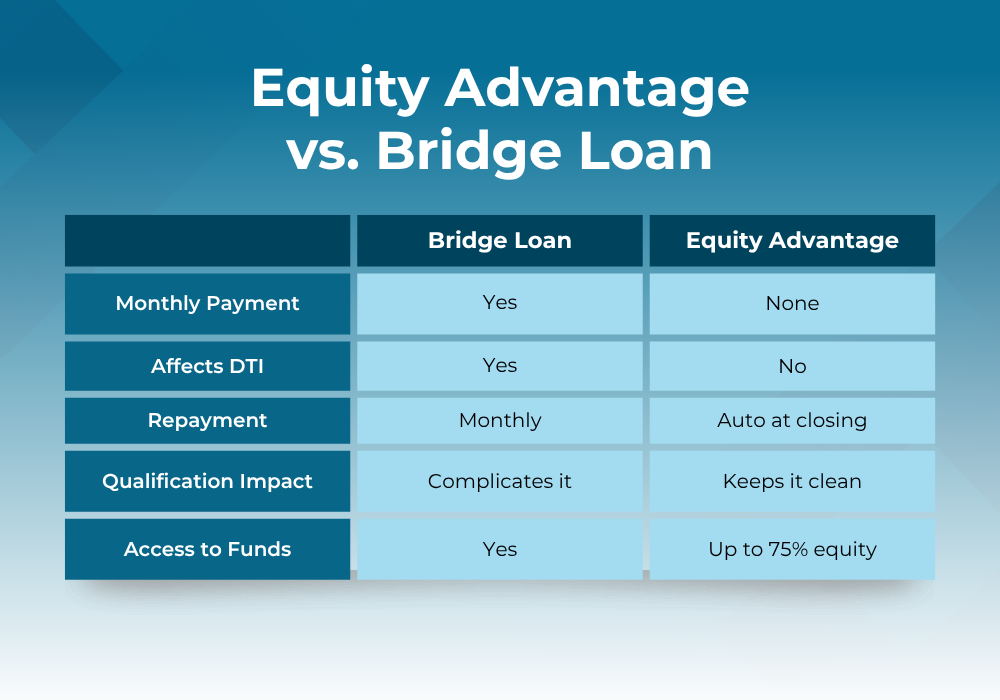

When buyers realize they need funds for a down payment before their current home sells, most assume a bridge loan is the only option.

A bridge loan is a short-term loan against your existing equity, designed to cover that gap. On the surface, it might sound like a clean solution.

In practice, it comes with real costs.

Bridge loans carry interest, require monthly payments, and show up as a new debt obligation on your file. That affects your debt-to-income ratio at exactly the moment you need your qualification to look clean for the new purchase.

For a lot of buyers, running those numbers is what sends them back to the sell-first condition instead.

Equity Advantage from Seattle's Mortgage Broker allows you to access up to 75% of your current home equity before it sells, with no monthly payment obligation while you own both properties.

The advance can be used toward your down payment, closing costs, staging expenses, moving costs, or any debt payoff that strengthens your buying position.

The full amount is repaid automatically through escrow when your current home closes and because there is no monthly payment, your debt-to-income ratio stays exactly where it needs to be for your new purchase qualification to remain clean.

Your down payment is fully funded, your transition costs are covered, and your monthly budget stays exactly where it was. That financial stability going into the purchase is what keeps your qualification clean and your offer competitive.

Your mortgage payments on the new home stay manageable from day one because nothing was added to your balance to fund the transition.

With your finances stable and your position secured, you're ready to make a competitive offer.

Think about what you've put together at this point.

Your equity is confirmed. A guaranteed buyer is already committed to your current home. Your down payment is fully funded without touching your monthly budget.

You're walking into an offer with critical variables already resolved. That preparation changes what your offer looks like on paper, and importantly, how a seller reads it.

Because the guaranteed buyer contract is already in place and the down payment is funded, the offer can go in without a home sale contingency attached. No sell-first clause. No language that signals the transaction depends on a second sale closing first.

What the seller receives is a purchase offer backed by a buyer who can close, fully funded, no conditions, no uncertainty about what happens next.

Sellers who received contingent offers before understand exactly what that uncertainty costs them, and they choose accordingly. In Seattle, that’s the single biggest structural advantage a buyer can have over another.

That structure also eliminates the risk of a kick-out clause being triggered. Without a contingency attached, there is nothing for the seller to kick out.

Rather than keeping the home on the market while a contingency window runs, the seller has every reason to move forward. When the offer is accepted, the focus shifts entirely to closing quickly and cleanly.

Because the Contingency Buster Program resolves the sell-first condition before you ever make an offer, there are no outstanding conditions slowing the process down on your end.

At Seattle's Mortgage Broker, paperwork and underwriting can be completed in under a week. By law a primary residence can't close in under two weeks, but the wait is on the clock, not on your file.

Flexible closing dates are an option, but timing the close at the end of the month helps avoid any overlap in mortgage payments.

The result is a direct move into your new home, no storage unit, no short-term rental, and no overlap where two households are running at the same time.

Once you're settled into the new home, your current property can go to market the right way: vacant, professionally staged, and without an immediate deadline forcing you to accept the first offer that comes in.

That distinction matters financially because staged homes statistically sell 33 to 50 percent faster and for 5 to 10 percent more than comparable unstaged properties, according to the National Association of Realtors' 2024 Profile of Home Staging.

On a Seattle home, a five percent premium is meaningful equity that follows you directly into the next chapter.

Selling without time pressure also means you can hold for the right offer rather than the fastest one, a position that lived-in, deadline-driven sellers almost never get to be in.

The sale of your current home feels like the finish line. In reality, it's the setup for one more financial win that helps you come out significantly ahead.

Once your current home sells, the remaining equity doesn't have to sit in a savings account.

Through Seattle's Mortgage Broker's Step Down Refinance Program, proceeds can be applied directly to your new mortgage balance.

A lower balance triggers a refinance that reduces both your interest rate and your monthly payment, without adding costs back onto your loan in the process.

A traditional refinance comes with Total Loan Costs including origination fees, processing, appraisal, title and settlement fees, and more, that can quietly add $6,000 or more to your loan balance every time you use it.

Stack that across two or three refinances, and the savings get eaten up before they ever reach your pocket.

The Step Down Refinance Program is built to eliminate that problem.

The Total Loan Costs associated with originating the loan are zeroed out or refunded at closing, what can't be waived gets refunded directly to you so that you net zero on loan costs every time.

That means you're not stacking thousands onto your balance each time rates drop. You're simply locking in a lower rate, resetting the amortization schedule, and keeping more of your money.

The program is designed to be used repeatedly. After six on-time payments, you're eligible to refinance again, as many times as the market supports it.

And when interest rates drop, even incrementally, the program is designed to let you act on it immediately rather than waiting for a drop large enough to justify a costly refinance.

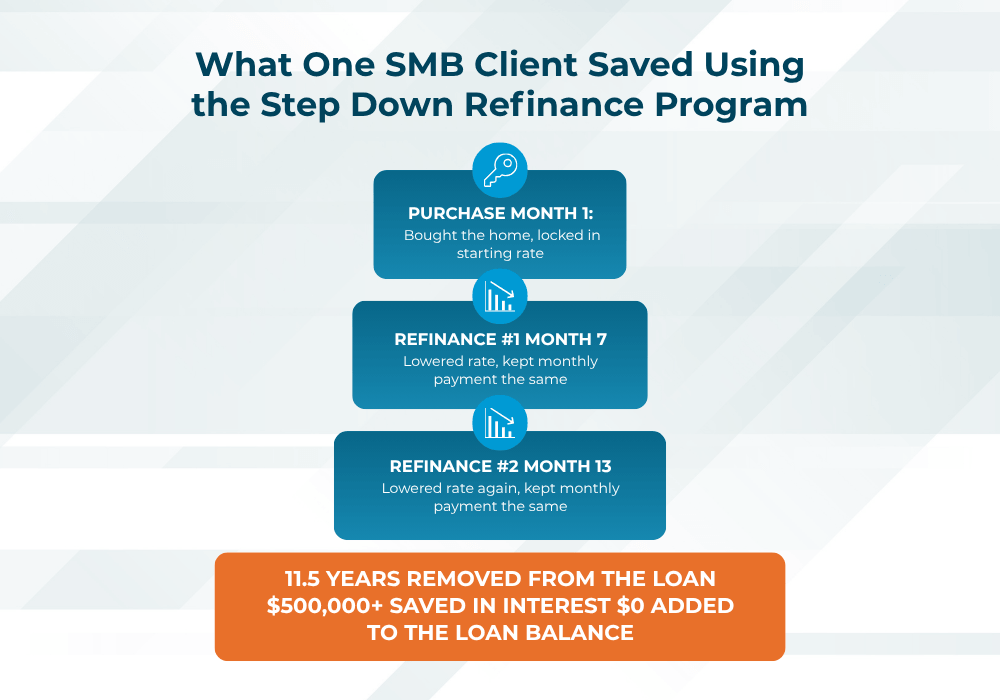

The math on this one is worth slowing down for. One SMB client completed three transactions in roughly 18 months, purchase, refinance, refinance. Each time, they chose to keep their monthly payment exactly where it was rather than pocket the monthly savings. The only thing that changed was how much time was left on the loan.

The result was eleven and a half years removed from their amortization schedule and more than half a million dollars saved in interest over the life of the loan.

What started as a move into a new home becomes a long-term interest reduction strategy built directly into the way your mortgage works.

Buying and selling at the same time in Seattle isn't complicated. It's just done in the wrong order by most people.

Flip the sequence and the whole picture changes.

The sell-first condition disappears from your offer. Your budget stays intact through the transition. The home you actually wanted is one you can compete for. And the equity from your sale goes back to work on your new mortgage, lowering your rate and cutting years off your loan.

That's the full picture of what this seven step process delivers.

One conversation is all it takes to confirm whether you qualify and map your path forward. Click here to get started.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)