How Seattle Agents Win More Listings With a Contingency-Free Buy Before You Sell Program

Read more

.webp)

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

You found the home. The price works. The neighborhood is right.

You make an offer, but then disaster strikes.

Despite your competitive bid, you lose out because your offer carried a condition the seller had no reason to accept.

That's the home sale contingency problem in Seattle's real estate market, and it plays out every week for buyers who are fully qualified but structurally disadvantaged the moment their offer hits the table.

Most buyers assume the sell-first condition is unavoidable if they haven't closed on their current home yet.

But it isn't. That condition is a variable you control, and removing it changes how sellers see your bid entirely.

Before you can remove it, however, it helps to understand what it costs you on the offer you're about to make and on the mortgage you'll carry for the next 30 years.

The conventional move for Seattle buyers trying to purchase a new home before they sell is a bridge loan, sometimes called a swing loan or gap loan.

The appeal is straightforward: short-term financing that covers the gap between your home purchase and your sale, funded against the equity in your existing home.

What the pitch glosses over is the qualification bar.

Borrowers typically need to meet a minimum credit score of 600 to 680, demonstrate stable income through pay stubs or tax returns, and keep a debt-to-income ratio below 50%. The part that eliminates more buyers than expected: you must qualify for both the bridge loan and the new home loan simultaneously.

That’s two full loan applications, two debt service obligations, all evaluated at the same time.

For a Seattle mortgage above $500,000, the math gets uncomfortable quickly. Bridge loan interest rates tend to run higher than traditional mortgage rates.

The term on most bridge loans runs six months to a year, with repayment terms that often include a large balloon payment at the end. If your existing home doesn't sell within that window, you're managing two mortgages with no resolution in sight.

Bridge loans provide fast access to capital, which matters in competitive markets where sellers expect certainty. But that speed comes at a price.

The new purchase mortgage comes in at a rate shaped by timing pressure, not optimal market conditions. If you enter that mortgage without a follow-on strategy, the rate you locked under the deadline becomes your default for years, not months.

Every month you carry an above-market rate past the first eligible refinance window is interest permanently paid, not a gap a future refinance can recover retroactively.

This is the hidden cost most bridge loan borrowers don't see coming. The short-term solution solves the immediate timing problem while creating a long-term issue that ends up costing homeowners.

Beyond the interest rate exposure, a standard bridge loan carries its own set of upfront costs.

Origination fees, appraisal requirements, and closing costs all add up on a product you're using for less than a year.

Bridge loan lenders require appraisals on the existing property used as collateral, and those fees are due regardless of how quickly your current home sells.

Then there's the monthly payment structure. Bridge loans typically allow for interest-only payments during the loan term, with the principal due in a lump sum when the existing home sells. That means you're funding two mortgages simultaneously, even if one is interest-only.

For buyers whose budget was sized around a single payment, the gap between what they planned and what they're actually paying can be significant.

Borrowers who can't sell their current property in time face the further risk of paying two mortgages indefinitely, a cash flow problem that compounds the longer the existing home sits.

Before committing to a bridge mortgage loan, buyers in Seattle should understand what else is available, and the pros and cons of each.

A home equity loan allows homeowners to borrow against existing home equity in a lump sum, typically at lower interest rates and with longer repayment terms than bridge financing. However, it requires the existing home to already have substantial equity and demands stable income to qualify, but it avoids the dual-mortgage pressure that makes swing loans difficult to manage.

A home equity line of credit, or HELOC, offers a more flexible version of the same concept.

Rather than a lump sum, a home equity line gives borrowers access to a revolving credit facility against their existing property, with lower closing costs than most bridge loans and the ability to draw only what's needed. Bridge loan interest rates tend to exceed what a HELOC charges, which makes the home equity line a more cost-efficient option when time allows.

An 80-10-10 loan, also known as a piggyback loan, splits the purchase into two mortgages and a 10% down payment, letting buyers avoid private mortgage insurance while keeping the primary loan below conforming limits. It solves a different problem than a bridge loan but brings further complexity in examining and understanding the full picture of short-term financing options.

Personal loans represent another financing option in theory, though in real estate transactions above $500,000 they rarely cover enough ground to be practical. They may have no collateral requirement but often come with higher rates and shorter loan terms than secured alternatives.

Each of these bridge loan alternatives may offer something that a bridge loan doesn’t, but the problem is that none of them, including the bridge loan itself, removes the home sale contingency from your offer.

They fund the gap. They don't fix the structural problem that's costing buyers deals in competitive markets.

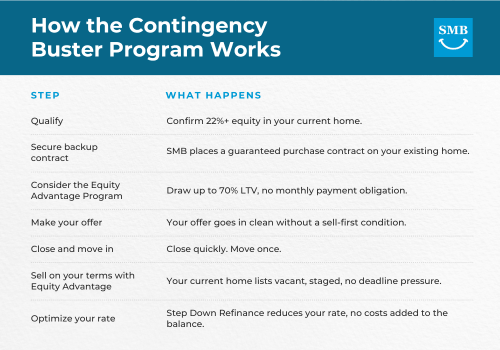

Seattle's Mortgage Broker built the Contingency Buster Program to solve the timing problem without the financial exposure a bridge loan carries.

Before you make an offer on the next home, Seattle's Mortgage Broker secures a guaranteed backup purchase contract on your current home. That contract means a committed buyer is already in place before your offer hits the table.

With that contract secured, your offer goes in without a home sale contingency. The seller receives a purchase offer backed by certainty, not a conditional deal that depends on a second transaction they can't control.

Seattle's Mortgage Broker closes quickly and allows you to compete directly with cash offers. That speed is what allows the backup purchase contract to function as the credible guarantee a seller needs to accept the offer.

Realtors across Seattle can also use this program with their clients, specifically because it delivers a contingency-free offer without the financial complexity a bridge loan introduces.

The program solves the timing problem by removing the condition, not by layering on additional debt.

The most common reason buyers reach for bridge financing is because they need to fund the down payment and cover transition costs before their current home sells.

Equity Advantage is the feature within the Contingency Buster Program built specifically for that purpose, and it works differently than any bridge loan alternative on the market.

The program removes three specific obstacles a bridge loan leaves in place:

Buyers can access up to 70% LTV of their current home's existing home equity before it sells. The advance carries zero monthly payment obligation during the transition, there's no interest-only payment, no second loan running against your budget, no impact on your debt-to-income ratio.

The full amount is repaid through escrow when your current property closes, repaid in a single lump sum from the sale proceeds with no payment schedule to manage in between.

That advance can go toward the down payment, closing costs, staging, renovations, moving expenses, or debt payoff to strengthen qualifications before the new home purchase.

There are no restrictions on use. And because there's no payment obligation, the buyer's cash flow stays exactly where it was throughout the transition, no budget pressure, no mortgage payment juggling, no financial stability concerns during the move.

Compare that to what a bridge loan requires: dual qualification, bridge loan interest rates higher than traditional mortgages, monthly payments on a short-term loan, and a balloon repayment at the end.

Equity Advantage is designed to do what gap financing does, bridge the gap between home purchase and sale, without any of the cost structure or qualification complexity that makes most bridge loans a difficult tool to use well.

The financial exposure that defines the bridge loan experience isn't present in this structure.

Once your current home sells and the equity is settled, the rate on the new mortgage is the decision that determines long-term financial outcome.

That's where the Step Down Refinance program becomes the third leg of the strategy.

Seattle's Mortgage Broker has a client who completed a purchase followed by two refinances in roughly eighteen months. That client chose to hold the monthly payment steady throughout and compress the amortization schedule instead of reducing the payment. The result: 11.5 years removed from the loan term and more than $500,000 in lifetime interest eliminated.

That outcome was possible because each refinance carried zero added cost to the loan balance.

The total loan costs, processing, appraisal, credit, title, settlement, were zeroed out or refunded at closing. With no recoup period required between refinances, the client was able to act every six months as rates moved, compounding savings that no single perfectly-timed refinance could have delivered.

The conventional "save 1% before refinancing" benchmark exists because a standard refinance carries $6,000 or more in total loan costs that have to be offset before the math makes sense.

When those costs are eliminated, the threshold for acting drops dramatically. A smaller rate improvement justifies acting sooner. Acting sooner means the rate drops faster. The interest that would have compounded at the higher rate for another year simply doesn't.

The Step Down Refinance is a post-sale optimization that can combine with the Contingency Buster Program, so that the purchase decision and the rate strategy are designed together, not assembled after the fact.

The best time to solve a contingency problem is before you make an offer. The best time to solve a rate problem is before you close on the loan.

Most buyers deal with both after the fact, scrambling for a bridge loan when the timing gets tight, then sitting on an above-market rate waiting for a refinance that makes financial sense by someone else's math.

You don't have to enter the purchase that way.

One conversation with Seattle's Mortgage Broker confirms whether you qualify for the Contingency Buster Program and shows you exactly what a clean, competitive offer looks like for your situation, before you need it.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)