How Do You Buy Another House Before Selling Yours Without Losing $40K?

Read more

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

The right home in Seattle doesn't sit on the market and wait for you to figure out your finances.

It hits the listings on Thursday, runs an open house Saturday, and generates offers by Monday afternoon.

If you're a current homeowner, every dollar of your down payment is locked inside a property you haven't sold yet. By the time you list your existing home, prep it for showings, negotiate an offer, and clear closing, the home you actually wanted has been in someone else's possession for six weeks.

This is the squeeze most buyers in Seattle feel: You're not short on equity. You're short on sequencing.

The real question isn't whether you should buy a house before you sell your house. For most homeowners that's the only sequence that protects the offer and the sale.

The question is how to do it without sinking your home purchase offer with a home sale contingency or stacking two mortgage payments on top of each other while the old house sits.

There are three traditional answers: a contingent offer, a bridge loan, or a home equity line of credit. Each one solves part of the problem, but creates a new one in the process.

This article walks through where each option breaks down, then lays out the cleaner alternative most Seattle homeowners don't know exists.

Selling before you buy sounds responsible, but in Seattle's market, it's often the move that costs you the most.

Here's what actually happens when you sell first.

Your home goes under contract, and the moment it does, a clock starts ticking. You now have a fixed window to find your next home, negotiate an offer, clear inspections, and get to closing.

Miss that window, and you're not just inconvenienced. You're in temporary housing—a short-term rental, an extended stay hotel, or your in-laws' guest room—while you keep hunting for a house you actually want to live in.

That's one move to get out and another move to get in. Add a storage unit, the carrying costs of a transition that was supposed to be seamless, and the mental load of living in limbo. Suddenly, what felt like the "safe" choice to buy before you sell, feels like anything but.

The pressure doesn't stay contained to your living situation. It follows you into every showing, every offer, every negotiation.

When you're house hunting against a closing deadline, you stop looking for the right home and start looking for any home you can get under contract in time. Sellers and their agents pick up on that energy fast. A buyer with a hard deadline is a buyer who might bend on price, waive contingencies under duress, or accept terms they'd otherwise push back on.

Selling first doesn't just create logistical stress. It hands the seller leverage you didn't intend to give them.

Some homeowners try to soften the squeeze with a rent-back agreement, staying in their sold home for a set period after closing to buy extra time.

It helps, but rent-backs typically cap at 60 days, require the buyer of your old home to agree, and still leave you racing to get a new house under contract before that window closes.

An extended closing period buys similar breathing room with similar limits.

Both options treat the symptom. Neither fixes the actual problem, which is that selling first puts you on someone else's timeline in a market that rewards buyers who can move on their own.

If selling first doesn't work, the alternative is buying before selling.

Most homeowners default to one of three financing options to bridge the gap. Each has a real use case. Each also has a weakness that costs you in a competitive market.

A home sale contingency is a clause in your purchase contract that makes your offer to buy a new home dependent on selling your current one first.

If your existing home doesn't sell by a specified date or price, you can back out of the new purchase without penalty.

That sounds protective to you. But to a seller, it reads as risk.

In a competitive market, sellers prefer buyers without a home sale contingency, because those buyers can close on the timeline the seller wants without their financing depending on a third-party transaction.

When your contingent offer goes head-to-head with a clean offer at the same price, the clean offer almost always wins. Sometimes the clean offer wins at a lower price. The contingency is a tax you intend to pay to protect yourself, but the tax you actually pay is often getting the home you want.

A bridge loan is a short-term loan that uses the equity in your current home to fund the down payment on your new one, with the loan balance repaid when your existing home sells.

Bridge loans typically run six to twelve months. Some are structured as interest only payments during that window; others roll the interest into the payoff.

The mechanics work. The cost is the friction.

A bridge loan means qualifying twice, once for the bridge loan, once for the new mortgage, with a loan officer running the same income, debt to income ratio, and credit checks across two transactions.

You'll pay closing costs on the bridge loan plus closing costs on the new mortgage, and bridge loan interest rates run higher than standard mortgage rates because the lender is taking on short-term risk.

If your current home sells on schedule, a bridge loan is workable but expensive. If it doesn't, you're carrying two mortgages plus the bridge loan, and the carrying costs compound fast.

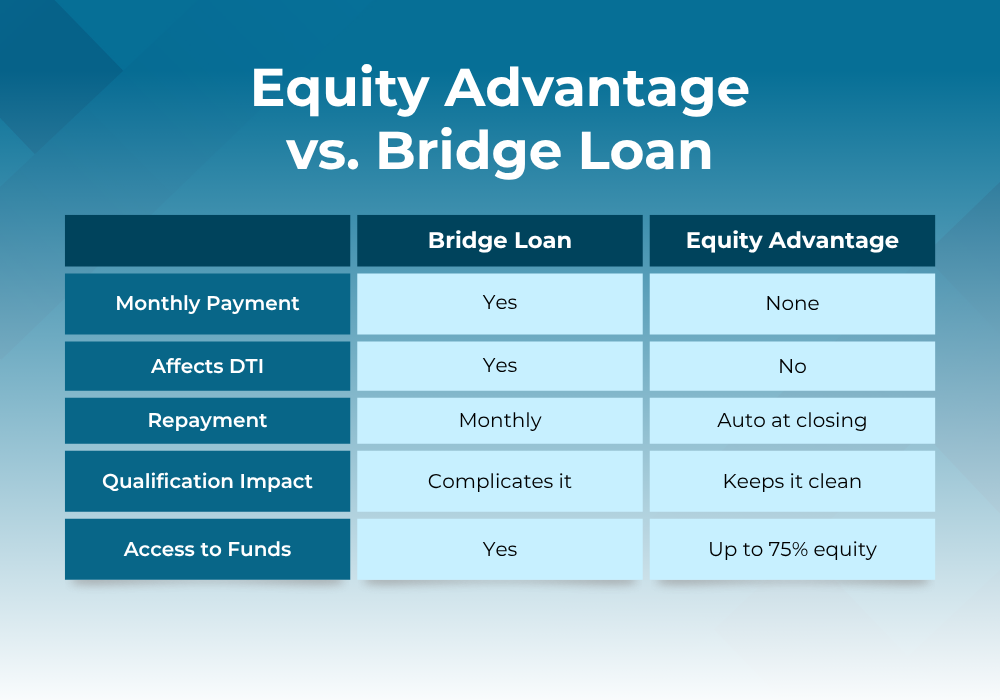

A home equity loan or home equity line of credit (HELOC) lets you borrow against your current home's equity to fund the down payment on the new house.

A HELOC gives you a draw period during which you can pull funds as needed; a home equity loan delivers a lump sum upfront.

Both are cheaper to originate than a bridge loan. Both add a second mortgage to your existing home, which means a second monthly payment until your existing home sells and the line is paid off.

Lenders also factor that second payment into your debt to income ratio when you apply for the new mortgage, which can cap how much house you qualify for or push you into a higher-rate loan tier.

A home equity line works best when you have significant equity, your personal finances absorb the temporary second payment without strain, and you're confident your current home will sell quickly. It works less well when any of those assumptions slip.

Look at the three options above and you'll notice something they all have in common.

Each one tries to solve the financing gap between buying and selling. None of them solves the actual problem: the contingency on the offer.

That's the part that's costing Seattle move-up buyers the homes they want.

A bridge loan funds your down payment. A HELOC gives you liquidity. But if your offer depends on selling your existing home, you're still asking a seller to hitch their transaction to one they can't see, can't control, and didn't sign up for.

The financing fix doesn't matter if the contingency is still sitting there in black and white.

The cleaner path is to eliminate the contingency before you ever write the offer, by securing a guaranteed buyer on your current home first.

That's the problem the Contingency Buster Program was built to solve.

Before you make an offer on your next home, Seattle's Mortgage Broker secures a guaranteed offer on the home you're leaving behind.

Your existing home is covered. Your next offer goes in clean; no sell-first clause, no contingency language, no reason for the seller to pass on you in favor of the buyer standing right behind you.

You're competing for the home you want, with an offer that reads like cash, without taking on a bridge loan or a second mortgage.

What that unlocks on both sides of the transaction is significant.

On the buy side, you're making a clean, cash-competitive offer a seller can take seriously without hesitation. On the sell side, you're keeping full control — selling staged, selling vacant, selling on your timeline, without the deadline pressure that pushes sellers into price concessions they didn't plan to make.

That's not a workaround. That's a different strategy entirely.

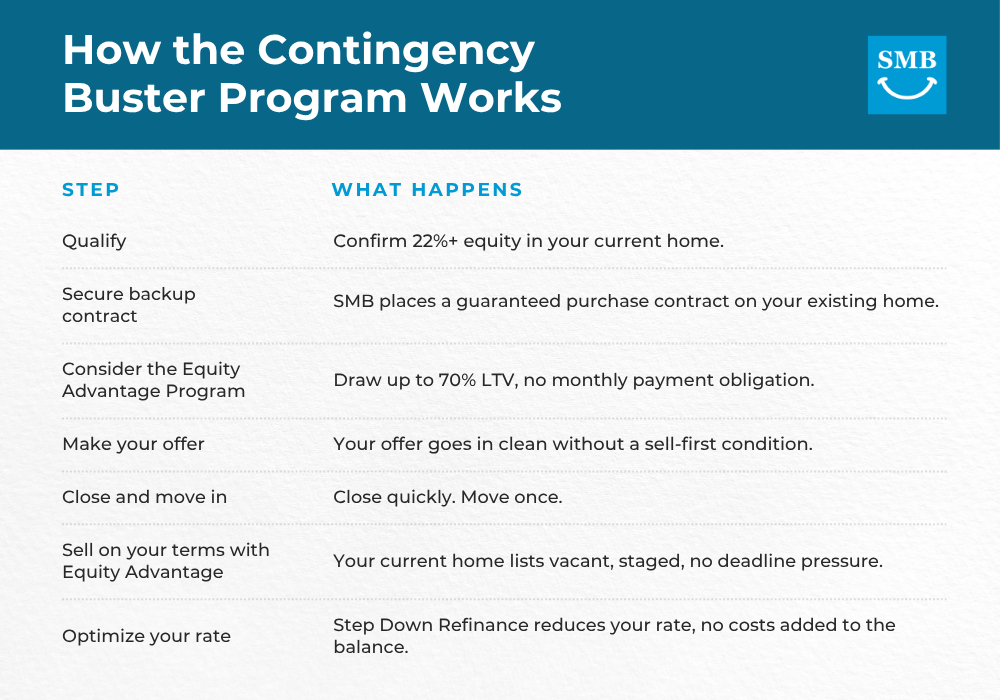

The program is built around the equity in your current home. There's no second mortgage, no bridge loan, and no need to qualify twice. The mechanics break down into five steps.

You need a minimum of 22% equity in your current home to go contingency-free. That's the threshold that allows the program to secure a guaranteed buyer in place on your existing home before you make your next offer. If you've owned your Seattle home for several years and made standard mortgage payments, you likely have significantly more than that, especially given how much regional home values have appreciated.

The qualification conversation is straightforward and built around your current home's equity, not a second loan or a second qualifying round.

Equity Advantage is an optional add-on that unlocks your current home's equity early, so your next offer is fully funded with nothing out of pocket.

It's a smarter alternative to a bridge loan. There are no monthly payments during the transition, and the advance is repaid automatically through escrow when your existing home sells. You don't qualify twice, you don't carry a second monthly payment, and you don't pay bridge loan rates. The funds are there when you need them and gone when you don't.

If you have significant equity and want to make the strongest possible offer with no cash flow strain in the meantime, Equity Advantage is the lever that gets you there.

Your offer goes in without a home sale contingency. No sell-first clause, no uncertainty about whether your financing will hold. To the seller and the seller's agent, your offer reads the same as a buyer who has already sold their previous home, or who's paying cash.

This is the leverage point. A clean offer at $850,000 routinely beats a contingent offer at $865,000 in Seattle's competitive real estate market, because sellers price certainty. The same dynamic that worked against you when you were the contingent buyer now works for you.

You close on your new home and move straight in. One move. No storage unit for the furniture you can't fit in a short-term rental. No extended stay hotel with a dog and two kids. No living out of boxes in a friend's spare room while you wait for the old house to close.

Avoid temporary housing altogether and get in your new home stress-free. Your old home sells the way every experienced real estate agent wishes every home could sell.

Vacant. Professionally staged. Photographed without your sectional blocking the fireplace or your kids' artwork covering the walls. Shown to buyers who can now picture themselves in it because nothing is in the way.

That's not a small thing.

According to the National Association of Realtors' 2024 Profile of Home Staging, vacant and professionally staged homes sell 33–50% faster and for 5–10% more than comparable unstaged listings. On a Seattle home priced at $1 million, that's an additional $50,000 to $100,000 in sale price that most homeowners leave on the table simply because they were still living there when it hit the market.

Most clients choose to list after they've moved for exactly that reason.

If your situation calls for listing earlier, that's always an option, but the staged-and-vacant approach almost always produces a stronger outcome, and the numbers back it up.

Once your existing home sells, you're not just closing a chapter, you're sitting on proceeds you can put to work.

That's where SMB's Step Down Refinance program comes in. Instead of letting that equity sit or disappear into a lump-sum payoff, you apply it to your new mortgage. The result is a lower rate, a lower monthly payment, and less total interest paid over the life of the loan.

This is the part of the program most people don't see coming, and the part that makes the whole thing click.

Think about where you started. You needed to buy a new home without losing it to a contingency, sell your current home without deadline pressure cutting into your price, and come out the other side in a better financial position than when you went in.

That's what Step 5 delivers. You bought the home you wanted with a clean, competitive offer. You sold your current home staged, vacant, and on your terms, for full value. And now you're using the proceeds from that sale to bring down the cost of the mortgage on the home you're already living in.

In Seattle's market, the buyer who can close without a sell-first condition wins. That buyer can be you, and it doesn't require a bridge loan or a HELOC to get there.

Qualifying takes one conversation. The program is built around the equity you've already earned in your current home, not a second loan or a second qualifying round. If the home you want is on the market right now, the time to know whether you qualify is before you write the offer, not after.

Book a strategy call with Seattle's Mortgage Broker to see if the Contingency Buster Program fits your situation.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)