How Seattle Agents Win More Listings With a Contingency-Free Buy Before You Sell Program

Read more

.webp)

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

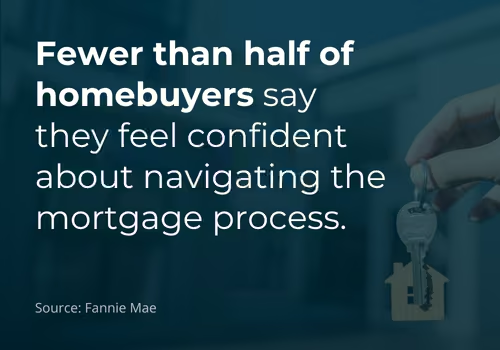

Homebuyers spend hours scrolling through listings, comparing neighborhoods, examining school districts, and even investigating the backsplash tile in a kitchen.

But when it comes time to decide how they’ll actually pay for that dream home?

They spend far less time weighing out their options.

Yet, your choice of lender affects almost everything to do with your home purchase: It impacts how many loan options you can compare, how smoothly the process goes, and how confident you feel from pre-approval to closing.

So, should you go with a bank or work with a mortgage broker?

This guide breaks down the differences and helps you decide which path makes the most sense for your homebuying journey.

When you're ready to buy a home, you'll likely need financing to make it happen.

From getting pre-approved to locking in a great interest rate, having someone guide you can make the whole process seamless.

Most buyers choose between two main financing options: getting a loan through a bank or working with a mortgage broker. Each offers a different experience, and understanding how they compare can help you decide which approach is best for your needs.

Let’s start by looking at each option and what it offers.

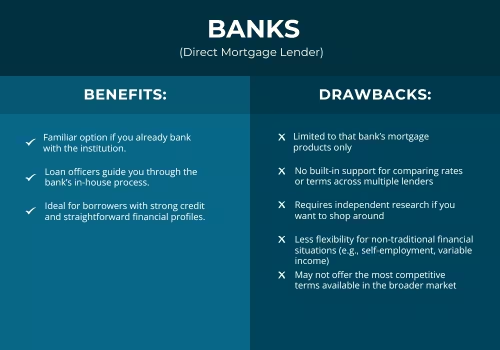

Banks and other financial institutions, like credit unions, act as direct lenders, offering mortgages through their own in-house lending programs.

These institutions often work alongside mortgage loan officers who help guide borrowers through the bank’s application and approval process.

When you apply directly, a loan officer will review your credit history, income, and financial history to determine what you qualify for.

Based on that, they’ll present you with one of their available mortgage products.

Getting a mortgage loan through a bank may be a good fit if you already have a relationship with the institution, have strong credit, or prefer a more traditional and familiar process.

While working with a bank or financial institution can be a good option for some buyers, there are a few limitations to consider.

Banks only offer their own mortgage products, so you won’t have access to a wider range of rates or terms unless you apply elsewhere. Because their focus is on in-house loans, you’ll need to do your own research if you want to compare options across lenders.

This approach can be less flexible if your financial situation is non-traditional. For example, if you’re self-employed or have variable income, it may be harder to get approved or find a loan that truly fits your needs.

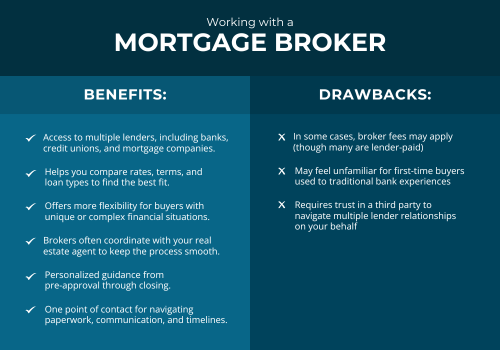

A mortgage broker, on the other hand, is a licensed professional who connects you with a wide range of lenders.

Their job is to compare rates, terms, and loan types across multiple sources—including banks, credit unions, and mortgage companies—then recommend the best fit based on your goals, credit, income, and long-term plans.

Instead of offering just one set of loan products, they help you explore several options based on your goals and financial profile.

This is especially helpful if you’re a first-time buyer, self-employed, or navigating a more complex financial situation.

Brokers often work closely with your real estate agent to keep things aligned and on schedule during the homebuying process. From pre-approval to closing, they guide you through each step and help you understand your options clearly.

Overall, mortgage brokers offer a more flexible and personalized experience, designed to give you options and support every step of the way.

Despite these advantages, there may be some drawbacks to consider.

For instance, there may be additional fees involved in certain situations. However, most brokers are paid by the lender, not the borrower.

For first-time buyers, the process may feel less familiar than working with a bank.

And while brokers present a range of options, it’s still important to ask questions and make sure the recommendations align with your long-term financial goals.

One of the key differences to understand is that mortgage brokers specialize solely in home loans, while banks offer a wide range of financial services.

This focus means that a broker’s full attention is on helping you find the mortgage that best fits your needs and financial situation.

Whether you're buying your first home or already own several properties, the mortgage process can feel overwhelming.

A good broker helps simplify each step, reduces the stress of managing the details, and gives you the clarity and confidence you need throughout your homebuying journey.

Here's how they do it:

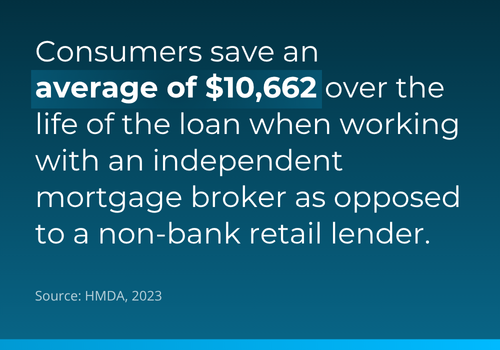

Instead of applying to one bank without any confirmation if there is a better offer out there, a broker checks rates and loan options from many different lenders including banks, credit unions, and alternative options you may not even know exist.

This gives you a broader view of what’s out there and helps you avoid overpaying or signing on to less favorable terms.

Mortgages come with a lot of fine print.

Your broker will break it all down, like how a fixed-rate loan compares to a variable one, or what different term lengths really mean for your monthly payments so you can make confident, informed choices.

From income documents to credit reports, applying for a mortgage means pulling together a lot of information.

A broker walks you through exactly what’s needed, helps you stay organized, and makes sure your application is complete and accurate.

Instead of juggling calls and emails from different banks, your broker takes care of all communication for you. They keep everything organized, follow up on your behalf, and make sure you’re updated at every step so nothing slips through the cracks.

A mortgage broker supports you through the entire home financing process.

If questions come up or unexpected issues pop up (and they often do), your broker steps in to troubleshoot and keep things on track.

Their goal is to make the process as smooth as possible so you feel supported, informed, and confident every step of the way.

Whether you're just starting to look or getting ready to sign the final documents, your broker is there to answer questions, solve problems, and make sure you’re set up for success at every stage.

Even with more buyers turning to mortgage brokers, some misunderstandings still come up.

Here’s what you should know about the most common mortgage broker myths.

In most cases, broker fees are paid by the lender, not by you.

If there is a fee involved, it’s usually minor and often offset by the savings they help you secure through better loan terms.

Mortgage brokers work with all kinds of borrowers, including those with excellent credit.

They’re especially helpful if you want to explore more options, if you’re self-employed, or if your financial situation is a little more complex than average.

Mortgage brokers are licensed and regulated professionals, often affiliated with a national association that upholds industry standards and ethical practices.

They are legally required to act in your best interest and are committed to providing transparency, education, and guidance so you can make confident, well-informed decisions.

Whether you're buying your first home or refinancing your fifth, a mortgage broker can offer the guidance, choice, and peace of mind that many buyers don’t get from traditional lenders.

If you're thinking about using a mortgage broker, it's helpful to know what the process looks like.

Brokers offer guidance, simplify complex decisions, and help you find a loan that fits your goals, not just your credit score.

Here’s what working with a mortgage broker typically includes:

Mortgage terms can be confusing. A broker explains your options in everyday language, helping you understand what each loan means for your budget and long-term plans.

Instead of dealing with multiple banks, you work with one person who handles communication, paperwork, and updates all in one place.

Whether you're self-employed, have non-traditional income, or are buying for the first time, brokers know which lenders offer more flexible solutions and which programs are in place for your situation.

Brokers often support clients after the sale too, like when it’s time to refinance or renew your mortgage down the road.

In many cases, working with a mortgage broker can make the process easier to navigate and more tailored to your individual needs.

But again, it’s not an easy decision.

Choosing how to finance your home is a big decision, and the right path depends on your goals, your comfort level, and your financial situation.

Asking a few key questions can help you figure out whether working with a mortgage broker makes sense for you:

If you answered yes to any of these, a mortgage broker could be the right fit.

Ultimately, the right choice comes down to what gives you the clearest path to move ahead with your home purchase.

Some buyers prefer the familiarity and structure of a bank. Others want the variety and personalized assistance that comes with a mortgage broker.

If you’re looking for clear answers, expert guidance, and a mortgage that aligns with your future plans, Seattle’s Mortgage Broker is here to help.

We’ll walk you through your options, compare lenders for you, and make sure you feel confident about every decision you have to make.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)